Supply hinders office recovery, but some states come out on top - RWC

Contact

Aug 8, 2023

Supply hinders office recovery, but some states come out on top - RWC

According to Vanessa Rader, Head of research, Ray White Commercial, the issue of “work from home” and the death of CBDs have dominated the headlines over the past few months.

-

Vanessa Rader, Head of research, Ray White Commercial.

Vanessa Rader, Head of research, Ray White Commercial. -

-

The issue of “work from home” and the death of CBDs have dominated the headlines over the past few months. Office occupancy levels have taken a dive in many markets as employers grapple with hybrid working styles becoming the new norm, while high supply continues to hamper some markets. As employers try to predict what the future office space looks like, the demand to occupy stock has fallen, however, some markets have been more affected than others.

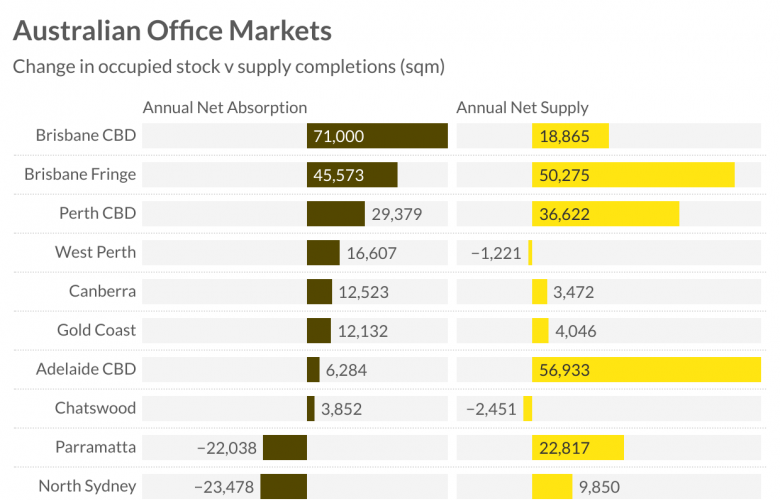

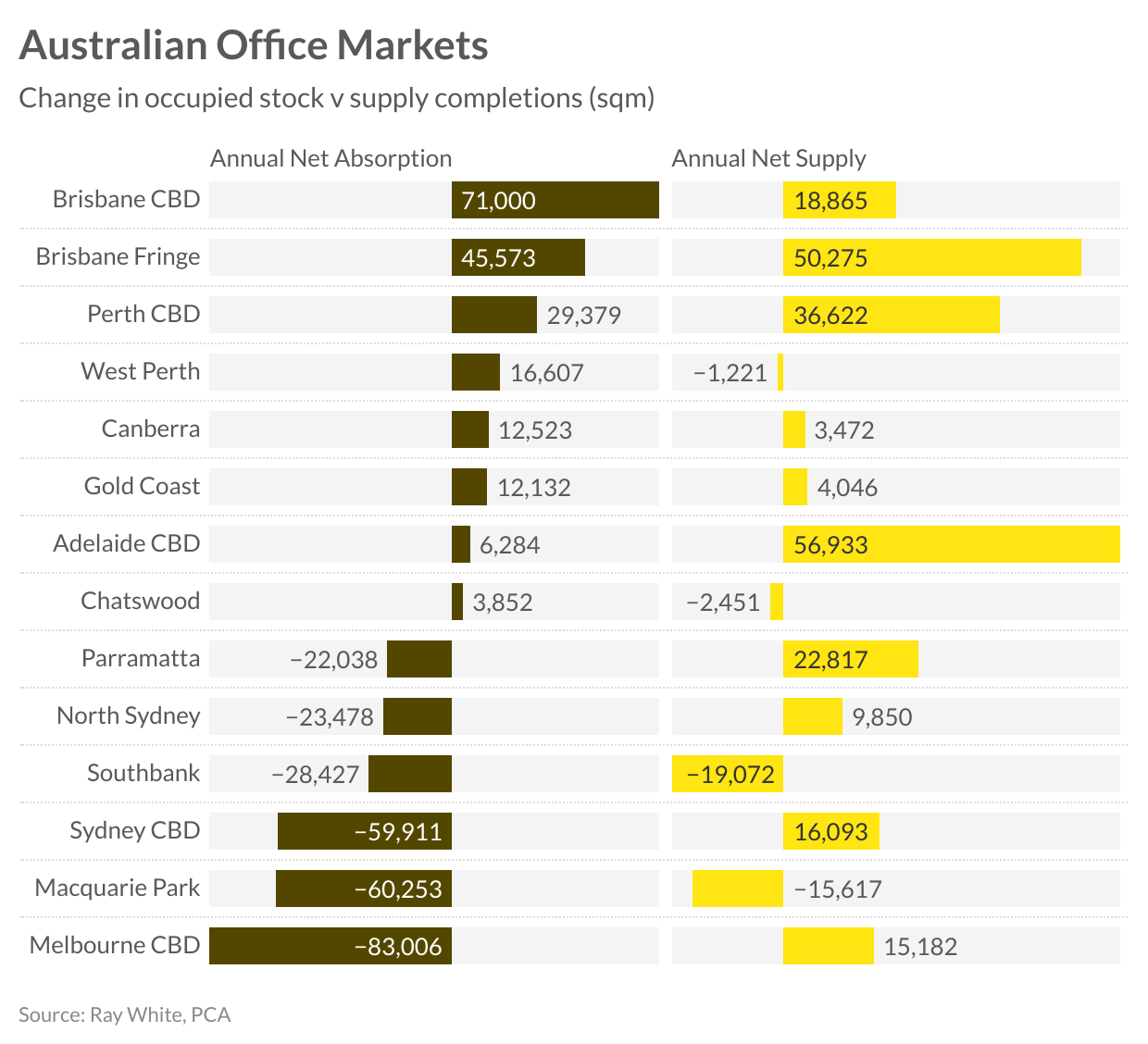

When considering the change in occupied stock or net absorption, it's clear that there has been a swing towards both Queensland and Western Australian markets. While Melbourne CBD has fared the worst, losing 83,000sqm of occupants over the last 12 months, Sydney CBD is not far behind at -59,911sqm. On the other end of the spectrum, Brisbane CBD has come out on top recording 71,000sqm of new activity over the year, after a number of difficult years for the CBD. Further adding to the Queensland story has been the reduction in “For Lease” signs across the Brisbane fringe, taking up 45,573sqm, and Gold Coast 12,132sqm.

Moving across the country, the rapid population growth in Western Australia has also spurred on the need for office space. Te Perth CBD has recorded 29,379sqm of new tenancies this past 12 months, while West Perth has been a quiet performer, increasing its occupancy by 16,607sqm.

It's important to note that net absorption of space is only half the equation for Australian office markets. The continued movement in stock levels plays a pivotal role in the health of an office market, impacting the overall vacancy level and in turn impacting rents, incentives and values of assets. For most markets, these strong levels of absorption have been overshadowed by a strong supply pipeline, adding office stock into the market and keeping vacancy levels elevated.

There has been much discussion on the volume of new stock completed and still in the pipeline for the Sydney and Melbourne CBDs, hampering their improvement, however, this development of new stock is not restricted to these states. While Brisbane CBD has been one of the only markets to see vacancy declines, it has enjoyed a combination of both strong take up and limited net supply additions of close to 19,000sqm. With more than 150,000sqm expected to be added to this market over the next few years, a prolonged high vacancy is anticipated. For markets such as Brisbane fringe and Perth CBD, impressive absorption of stock has been overshadowed by high new supply completions, resulting in the upward movement in vacancies.

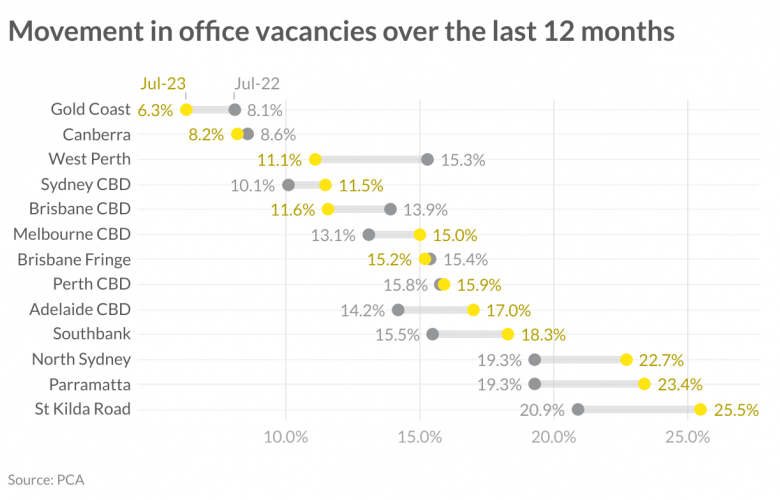

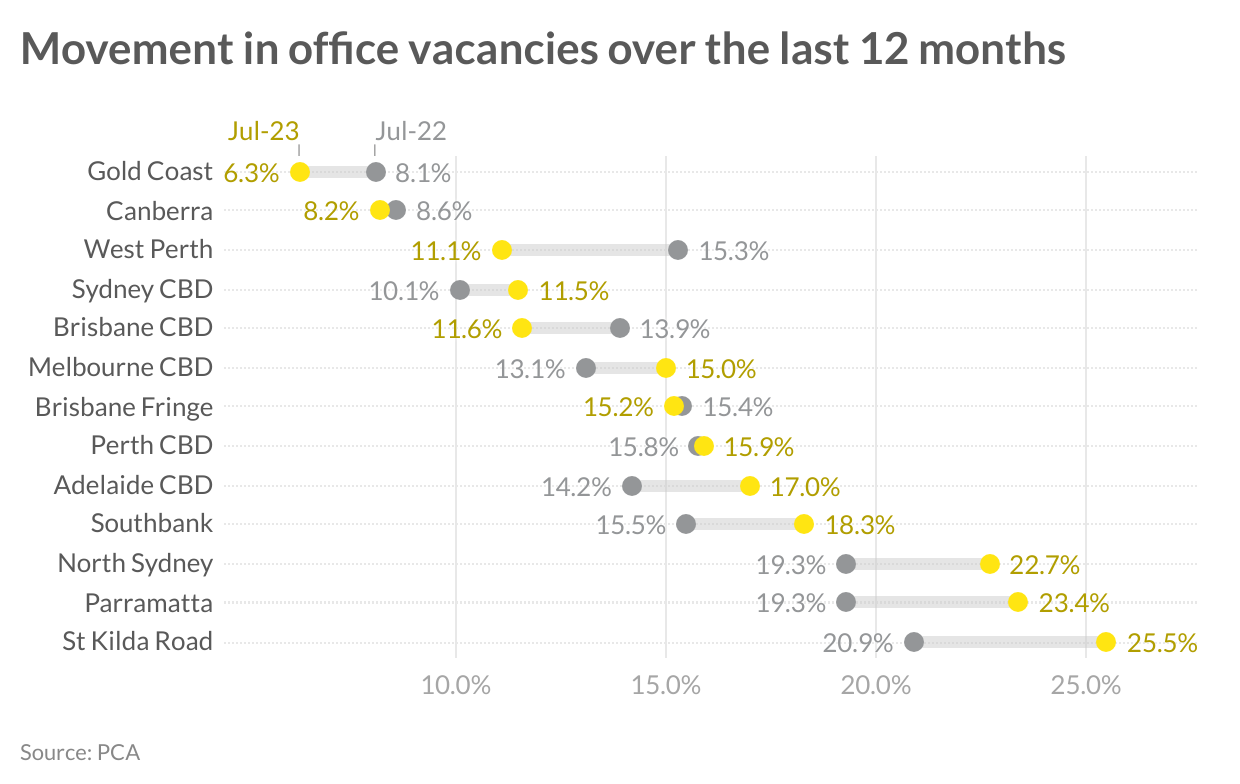

Markets such as Gold Coast and Canberra have had limited change to stock levels resulting in their favourable take up, reducing vacancies to 6.3 -per cent and 8.2 per cent respectively, the lowest vacancy markets in the six months to July 2023. West Perth has benefitted from both space contraction and new tenancies, reducing vacancy to 11.1 per cent, an eight-year low.

While both Sydney and Melbourne CBDs have had net supply additions, they have only represented 16,093sqm and 15,182sqm respectively, compared to the negative take up recorded, resulting in both cities seeing vacancy up lift to 11.5 per cent and 15 per cent. For many suburban markets such as Parramatta, Macquarie Park and North Sydney, new office completions have further hindered their recovery, with results moving the vacancy rates further upward creating a greater divide between prime and secondary assets.

Important Information:

Contact details:

Vanessa Rader

RWC

0432 652 115

Email

18366

17478

Vanessa Rader