Are offices still a premier investment opportunity?

Contact

Jun 6, 2023

Are offices still a premier investment opportunity?

According to Vanessa Rader, Head of research, Ray White Commercial, the office market has been through a tough few years, with COVID-19 changing the way tenants interact with offices, resulting in changing income profiles and demand for investment.

-

Insights by Vanessa Rader, Head of research, Ray White Commercial.

Insights by Vanessa Rader, Head of research, Ray White Commercial. -

-

The office market has been through a tough few years, with COVID-19 changing the way tenants interact with offices, resulting in changing income profiles and demand for investment. The prolonged elevated vacancy rate has done much to dampen investment activity in the once premier asset class, in particular CBD locations, which continue to be hampered by these reduced occupancy levels. Uncertainty by employers surrounding staff returning to work has seen many occupiers reduce their footprint or leave CBD locations, favouring suburban markets. So how will this impact offices as an asset class going forward?

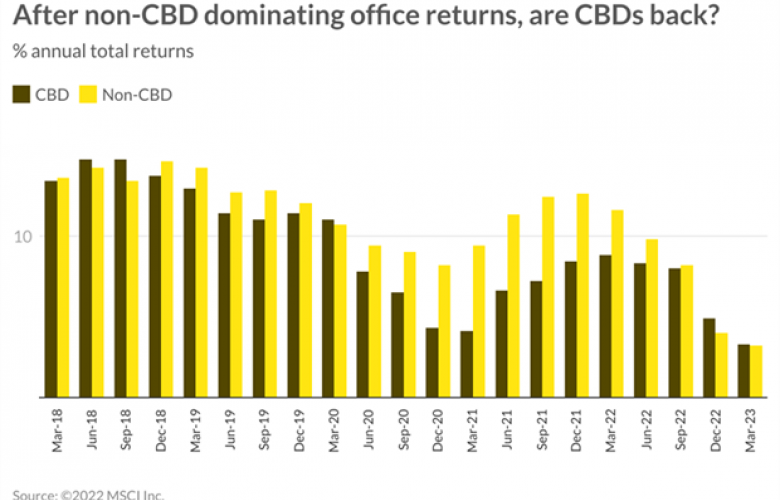

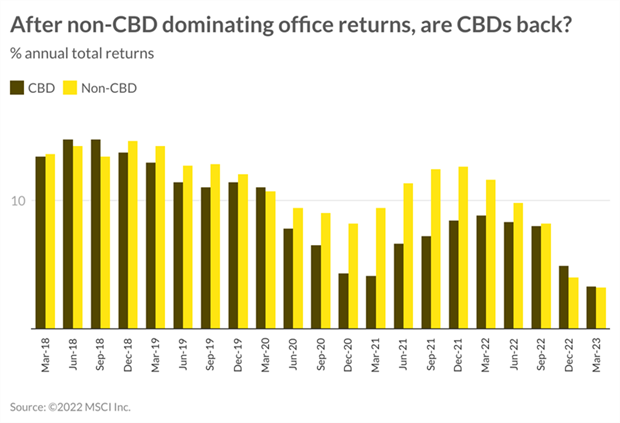

Taking a look back on the last three years, we have seen the growing attractiveness of non-CBD locations overtaking CBDs across Australia given their superior investment returns. Since the onset of COVID-19, returns did reduce, however, with lockdowns restricting staff from attending the office, we saw return levels reduce more prominently in CBD locations. Low interest rates and an appetite to invest in commercial property drove investment into office assets, however, returns for non-CBD offices outstipped those of CBDs due to substantial capital appreciation. Investment yields dropped to new lows with non-CBD locations having greater room to move and offer greater affordability compared to CBD assets, resulting in a narrowing of average yields. High inflationary pressures have seen income returns continue at a high rate, regardless of location, keeping total return levels positive despite interest rate increases over the last 12 months.

Over the last six months we have seen returns for CBDs outstrip those of non-CBDs with total returns for March 2023 recorded at 3.3 per cent and 3.2 per cent respectively. However, looking over the longer term, non-CBD results have outperformed over various time periods. The five-year average highlights CBD annual total returns at 8.0 per cent compared to non-CBD at 9.8 per cent, and even over the longer term (10 years) CBDs sit at 9.9 per cent while non-CBD locations averaged 11.1 per cent per annum. These results vary considerably across states, with March 2023 results for CBD ranging as low as -1.5 per cent total returns in Canberra, to 4.8 per cent for Brisbane CBD. Looking over a five-year average these rates vary from 6.3 per cent per annum in Perth CBD, through to 8.9 per cent for Melbourne CBD. Looking at non-CBD markets, total returns have been difficult for Parramatta down -0.7 per cent this period, however, over the last five years Parramatta averaged 9.5 per cent per annum ahead of North Sydney at 9.1 per cent per annum.

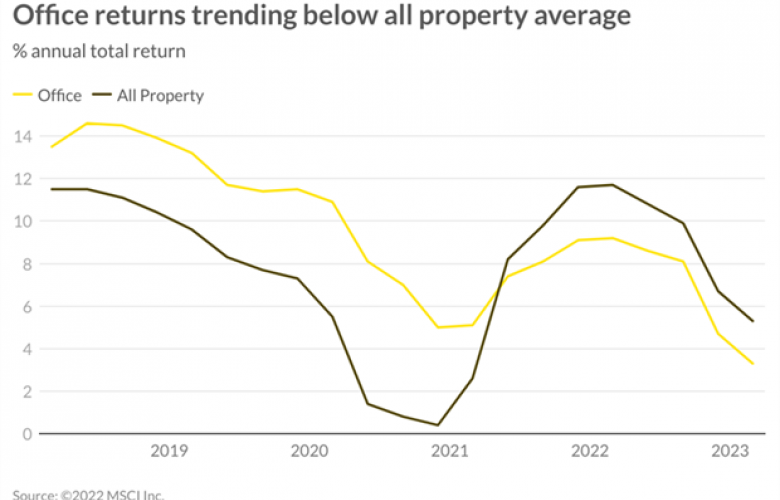

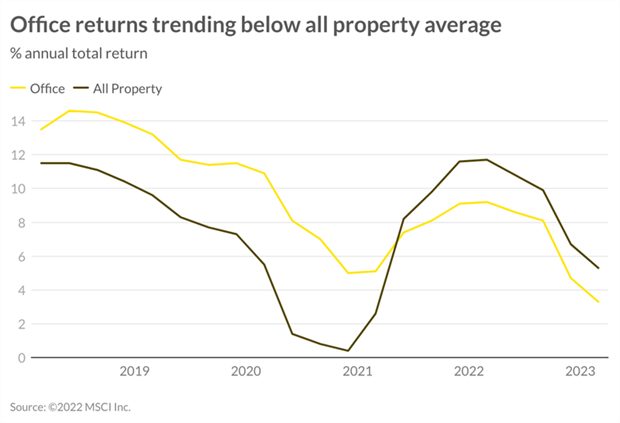

Prior to COVID-19, office assets were considered a premium commercial investment choice. High demand from offshore buyers in major CBDs was testament to the attractiveness of the asset class. Historically, office asset returns had outstripped those of the other major asset types, however, we saw a change in these results in mid-2021 where “all property” returns eclipsed those of office and office continues to maintain a discount to this rate. Currently (March 2023) “all property” returns sit at 5.3 per cent, propped up by a 4.8 per cent income return, while office assets see total returns of just 3.3 per cent, due to the decline in capital returns at -1.2 per cent, while income remains elevated at 4.5 per cent. The positive “all property” returns are aided by both industrial and retail, which have returns in excess of office results, industrial most notably up 10.4 per cent in total returns, despite being the lowest rate recorded for the industrial market since September 2017.

Return prospects are appearing to now favour other asset classes such as industrial and retail, and uncertainty remains over the longevity of the office market during this tight labour period resulting in prolonged flexible working conditions. There may be some pause in major office transactions with purchasers more considered of their expected returns and movements in capital values, however, the trophy nature of our CBDs, in particular Sydney and Melbourne, will still draw investment, particularly given the limited nature of larger institutional grade industrial assets and the caution also surrounding future for retail.

Insights by Vanessa Rader, Head of research, Ray White Commercial.

Related Reading:

Retail returns propped up by inflationary pressures on income

What are commercial investors buying this year?

Industrial remains the leading performing commercial asset class

Trophy Ascot supermarket by Ray White’s Retail Investment Team - withstands cash rate pressure

Important Information:

Contact details:

Vanessa Rader

RWC

0432 652 115

Email

18231

17478

Vanessa Rader